AI for quantitative finance

Published:

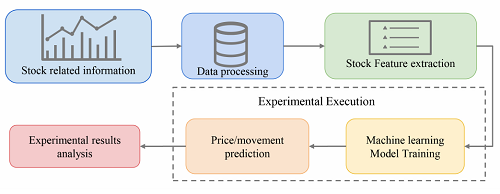

## Introduction Quantitative finance technologies have become pivotal in shaping modern financial markets,transforming how investment decisions are made and traded.In this domain,deep learning has emerged as a powerful tool,reshaping traditional quantitative analysis and strategies.Deep learning's ability to process vast amounts of data,identify complex patterns and optimize trading decisions has made it indispensable in the financial world. Quantitative finance encompasses a broad spectrum of activities,from algorithmic trading and risk management to portfolio optimization and market forecasting.The application of deep learning in these areas has not only enhanced the efficiency and precision of financial operations but also opened up new avenues for innovation. ## Quantitative Finance Tasks and Deep Learning Models ### Key Tasks in Quantitative Finance Quantitative finance involves several key tasks,each with its own set of challenges and objectives.These include: • Algorithmic Trading.Developing automated trading systems that can execute trades at optimal times based on market conditions and predefined strategies. • Risk Management.Creating models to assess and mitigate financial risks associated with investments and trading activities. • Portfolio Optimization.Selecting the best mix of assets to maximize returns while minimizing risks. • Market Forecasting.Predicting future market trends and price movements to inform investment decisions. Deep learning models have been applied to all these tasks,with varying degrees of success. ### Recurrent Neural Network (RNN) Based Models RNNs have been widely used in quantitative finance due to their ability to process sequential data,such as time series of stock prices and trading volumes.Their variants like LSTM and GRU have shown significant improvements in capturing long-term dependencies in financial data. For example,Akita et al. [1] proposed a method combining paragraph vectors and LSTM to predict stock prices by leveraging textual information from news articles and financial reports.Their model demonstrated superior performance compared to traditional methods like MLP and SVR. ### Convolutional Neural Network (CNN) Based Models CNNs have shown great promise in processing structured data and extracting meaningful features.Despite being primarily used in image recognition tasks,CNNs have also been applied to financial data with remarkable results. The Universal CNN-based predictor (U-CNN Pred) [47] is a notable example.It uses a layer-wise pre-training approach to build a model structure that is both effective and less prone to overfitting due to its shallow architecture. ### Reinforcement Learning (RL) Models RL has gained increasing attention in quantitative finance for its ability to model the interaction between an agent (trader) and the environment (financial market).The agent learns to make optimal trading decisions by maximizing cumulative rewards. The REINFORCE algorithm [135] is a basic policy gradient method that has been used to optimize trading strategies by directly updating the policy based on the rewards received from the environment. ## Datasets and Model Input Features The performance of deep learning models in quantitative finance is heavily dependent on the quality and relevance of the input data.Various types of data are used in these models,including: • Stock Prices and Indices.The most direct reflection of market performance,used as both input features and prediction targets. • Technical Analysis Tools.Indicators like exchange rates,book-market ratios and trading volumes that are strongly correlated with market performance. • Macroeconomic Data.Indices such as the Consumer Price Index (CPI) and Gross Domestic Product (GDP) that provide insights into the overall economic conditions. • Fundamental Data.Comprehensive information about a company's financial conditions and structure. • Textual Information.News articles,reports and social media posts that can influence investor sentiment and market trends. The integration of these diverse data sources has been shown to enhance the predictive power of deep learning models in quantitative finance. ## Evaluation Metrics The evaluation of deep learning models in quantitative finance involves various metrics that assess the accuracy and effectiveness of predictions.These include: • Accuracy-based Metrics.Precision,recall and F1-score are commonly used to evaluate the performance of classification models. • Error-based Metrics.Mean Absolute Error (MAE),Root-Mean-Square Error (RMSE) and Mean Absolute Percentage Error (MAPE) are used to measure the discrepancy between predicted and actual values. • Return-based Metrics.Internal Rate of Return (IRR),Average Annual Return (AAR) and Sharpe Ratio (SR) are used to evaluate the profitability and risk-adjusted performance of investment strategies. These metrics provide a comprehensive framework for comparing and selecting the best-performing models in different quantitative finance tasks. ## Future Directions and Open Issues Despite the significant progress made in applying deep learning to quantitative finance,several challenges and open issues remain. • Improving Generalization Ability.Enhancing the ability of models to perform well on unseen data and adapt to changing market conditions. • Integrating Deep Learning with Online Learning.Developing methods that can continuously update and optimize models in real-time as new data becomes available. • Enhancing Evaluation and Datasets.Establishing unified evaluation criteria and benchmark datasets to facilitate more consistent and comparable research. • Leveraging Distributional RL for Stock Trading.Exploring the potential of distributional RL to better balance profit and risk in trading algorithms. • Addressing Partially Observable Markov Decision Process.Devising strategies to handle the partial observability of financial markets and improve the robustness of RL-based trading systems. ## Conclusion This survey has provided a comprehensive overview of the application of deep learning in quantitative finance. We have explored the key tasks in quantitative finance,discussed various deep learning models and their applications,and highlighted the challenges and future directions in this exciting field. Through this survey,we aim to equip researchers and practitioners with a solid understanding of the current state of deep learning in quantitative finance and inspire further innovation and advancement in this domain.

## Introduction Quantitative finance technologies have become pivotal in shaping modern financial markets,transforming how investment decisions are made and traded.In this domain,deep learning has emerged as a powerful tool,reshaping traditional quantitative analysis and strategies.Deep learning's ability to process vast amounts of data,identify complex patterns and optimize trading decisions has made it indispensable in the financial world. Quantitative finance encompasses a broad spectrum of activities,from algorithmic trading and risk management to portfolio optimization and market forecasting.The application of deep learning in these areas has not only enhanced the efficiency and precision of financial operations but also opened up new avenues for innovation. ## Quantitative Finance Tasks and Deep Learning Models ### Key Tasks in Quantitative Finance Quantitative finance involves several key tasks,each with its own set of challenges and objectives.These include: • Algorithmic Trading.Developing automated trading systems that can execute trades at optimal times based on market conditions and predefined strategies. • Risk Management.Creating models to assess and mitigate financial risks associated with investments and trading activities. • Portfolio Optimization.Selecting the best mix of assets to maximize returns while minimizing risks. • Market Forecasting.Predicting future market trends and price movements to inform investment decisions. Deep learning models have been applied to all these tasks,with varying degrees of success. ### Recurrent Neural Network (RNN) Based Models RNNs have been widely used in quantitative finance due to their ability to process sequential data,such as time series of stock prices and trading volumes.Their variants like LSTM and GRU have shown significant improvements in capturing long-term dependencies in financial data. For example,Akita et al. [1] proposed a method combining paragraph vectors and LSTM to predict stock prices by leveraging textual information from news articles and financial reports.Their model demonstrated superior performance compared to traditional methods like MLP and SVR. ### Convolutional Neural Network (CNN) Based Models CNNs have shown great promise in processing structured data and extracting meaningful features.Despite being primarily used in image recognition tasks,CNNs have also been applied to financial data with remarkable results. The Universal CNN-based predictor (U-CNN Pred) [47] is a notable example.It uses a layer-wise pre-training approach to build a model structure that is both effective and less prone to overfitting due to its shallow architecture. ### Reinforcement Learning (RL) Models RL has gained increasing attention in quantitative finance for its ability to model the interaction between an agent (trader) and the environment (financial market).The agent learns to make optimal trading decisions by maximizing cumulative rewards. The REINFORCE algorithm [135] is a basic policy gradient method that has been used to optimize trading strategies by directly updating the policy based on the rewards received from the environment. ## Datasets and Model Input Features The performance of deep learning models in quantitative finance is heavily dependent on the quality and relevance of the input data.Various types of data are used in these models,including: • Stock Prices and Indices.The most direct reflection of market performance,used as both input features and prediction targets. • Technical Analysis Tools.Indicators like exchange rates,book-market ratios and trading volumes that are strongly correlated with market performance. • Macroeconomic Data.Indices such as the Consumer Price Index (CPI) and Gross Domestic Product (GDP) that provide insights into the overall economic conditions. • Fundamental Data.Comprehensive information about a company's financial conditions and structure. • Textual Information.News articles,reports and social media posts that can influence investor sentiment and market trends. The integration of these diverse data sources has been shown to enhance the predictive power of deep learning models in quantitative finance. ## Evaluation Metrics The evaluation of deep learning models in quantitative finance involves various metrics that assess the accuracy and effectiveness of predictions.These include: • Accuracy-based Metrics.Precision,recall and F1-score are commonly used to evaluate the performance of classification models. • Error-based Metrics.Mean Absolute Error (MAE),Root-Mean-Square Error (RMSE) and Mean Absolute Percentage Error (MAPE) are used to measure the discrepancy between predicted and actual values. • Return-based Metrics.Internal Rate of Return (IRR),Average Annual Return (AAR) and Sharpe Ratio (SR) are used to evaluate the profitability and risk-adjusted performance of investment strategies. These metrics provide a comprehensive framework for comparing and selecting the best-performing models in different quantitative finance tasks. ## Future Directions and Open Issues Despite the significant progress made in applying deep learning to quantitative finance,several challenges and open issues remain. • Improving Generalization Ability.Enhancing the ability of models to perform well on unseen data and adapt to changing market conditions. • Integrating Deep Learning with Online Learning.Developing methods that can continuously update and optimize models in real-time as new data becomes available. • Enhancing Evaluation and Datasets.Establishing unified evaluation criteria and benchmark datasets to facilitate more consistent and comparable research. • Leveraging Distributional RL for Stock Trading.Exploring the potential of distributional RL to better balance profit and risk in trading algorithms. • Addressing Partially Observable Markov Decision Process.Devising strategies to handle the partial observability of financial markets and improve the robustness of RL-based trading systems. ## Conclusion This survey has provided a comprehensive overview of the application of deep learning in quantitative finance. We have explored the key tasks in quantitative finance,discussed various deep learning models and their applications,and highlighted the challenges and future directions in this exciting field. Through this survey,we aim to equip researchers and practitioners with a solid understanding of the current state of deep learning in quantitative finance and inspire further innovation and advancement in this domain.